How to Buy a Car With Money Owing - The Definitive New Zealand Guide

Our guide explains the risks involved with buying a car with finance owing, how to check the PPSR, steps to protect your money, words of warning from previous buyers and FAQs.

Updated 1 April 2024

Summary:

-

A car with "money owing" or "finance debt" means that the owner has finance on the car. For example, they may have it for sale for $10,000 and owe their lender $7,000 - who to pay (and how to do it) can be risky without a proven process.

-

While social media posts (such as these Reddit threads from 2020 and 2021 warn buyers to avoid cars for sale with finance owing, many people go ahead anyway. What matters is that you follow a process that protects you and ensures the car's ownership transfers without debt.

-

Sellers should always advertise their cars with 'finance owing' or similar; not doing this is unhelpful and somewhat dodgy. Generally, if a seller has agreed on a price and then you find out there is money owing, it's arguably best to disregard everything else the seller has told you about the car's history and known issues. You may be dealing with a problematic seller.

-

Warning: If the seller causes any problems or you sense something isn't right during the buying process, we suggest you walk away. The risks can be high, and you don't want to be left without a car, having paid a seller.

How do most people buy a car with finance owing? The most common approach follows these steps:

- You find out how much debt is owed from a settlement statement, issued by the lender. An example of what this looks like can be downloaded here.

- You pay the seller the sale price you've agreed upon minus the debt owing amount.

- Then, once ownership is yours, you pay the finance directly to the lender.

Our View: We believe you never pay the finance before getting ownership of the car because the seller could stop talking to you if you pay the lender first. Paying the seller the difference between the sale price and the debt owed handles their 'equity' ownership while you take direct responsibility and settle the debt. If you don't do this, the seller may take your money and run; the loan will default, and your car will be repossessed.

Important: Never ask the seller to pay off the finance from the money you pay them - they have no obligation to do this and may pocket the money. You'll get the car, but if the debt is still owed, then the car will be repossessed. You must pay the lender directly.

To help explain everything you need to know to protect your money, our guide covers:

- Understanding the Risks

- How to Use the Personal Property Securities Register (PPSR) to Check for Debt if You're Buying a Car

- Dealing with Sellers - What You Need to Know and Do

- Buying a Car and Paying Off the Seller's Finance: Our Step-by-Step Guide to Protect Your Money

- Words of Warning from New Zealanders Who Have Bought Cars with Finance Owing

- Frequently Asked Questions

How can I check if a car has finance owing?

You can log into the PPSR (Personal Property Security Register) and check the car's registration - we've outlined this process here. If the vehicle has money owed, it will be mentioned.

Why is following the right process so important? A Car Loan Expert user who wanted to remain anonymous shares his experience as a warning:

"Buying a car with finance was a disaster and left me burned. The payment I made to the seller was supposed to cover the loan settlement. I paid because I assumed the loan would be cleared. However, it was a lie - the seller used most of the money for personal needs, only paying a fraction towards the loan. I ended up with a car still under finance, and it was a legal hassle to get it resolved. This experience taught me that you pay lenders directly and the seller last".

Understanding the Risks

When you buy a car with finance owing, you're essentially stepping into a situation where, unless you manage it correctly, the car is the security for a loan that hasn't been fully paid off. Such a situation has several risks and implications:

- The risk of repossession: If the previous owner's debt isn't settled after you pay the seller, the finance company will eventually repossess the car from you because the car is the security for the loan. While the debt won't be in your name, your car is liable for the debt.

- Uncertain ownership rights: Your car ownership isn't clear until the finance is prepaid. You may own the car per NZTA records, but until the debt is fully paid, the finance company typically holds an interest in it.

- Joint ownership complications: If the car you're buying is jointly owned, both parties must consent to the sale. Without this, the sale might be legally challenged later, complicating your ownership even if any debt has been repaid.

Car finance is often flagged in online listings; we list examples on Trade Me below to illustrate what it looks like:

How to Use the Personal Property Securities Register (PPSR) to Check for Debt if You're Buying a Car

The PPSR is your starting point, and our guide to the PPSR and car loans comprehensively covers this important check.

To search the PPSR, you need to register. Once you've set up your profile, you can search for Motor Vehicles, Debtor Persons, Debtor Organisations, Aircraft, and Financing Statements.

This video explains the setup and functionality. To search to see if there is debt owed on a motor vehicle, you need to follow the steps:

- Log in to the PPSR.

- From the dashboard, choose the motor vehicle search.

- Confirm that you are searching for a legitimate reason (which is required by law).

- Enter your search criteria. You'll enter the vehicle's Registration Number, Vehicle Identification Number (VIN), and/or Chassis Number.

- Use a credit or debit card to pay the search fee - $2 (plus GST).

- View, email, print or download the search results.

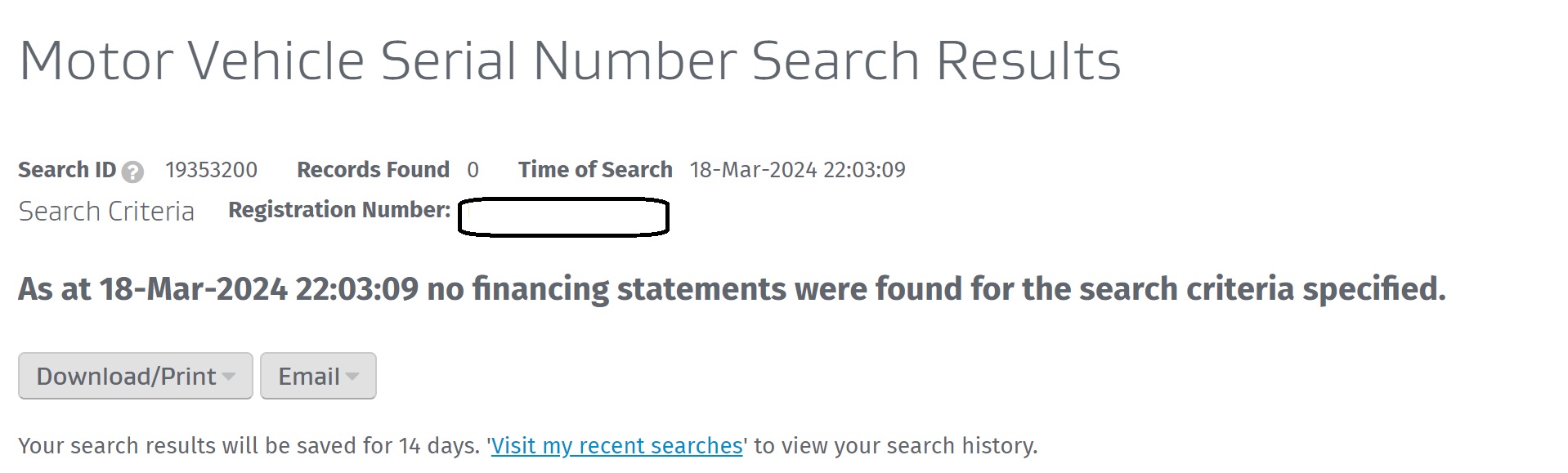

If finance is owed, you'll get a report that looks like this, but it won't tell you how much money is owed.

If there's no finance owing, the PPSR website will confirm this in a format like the below:

CarJam vs the PPSR - What option should I use?

- CarJam and the PPSR website both offer searches to identify if there are security interests on a car, e.g. if any finance is owed. Neither report tells you the balance of the debt.

- Both websites are quick and easy to use, although CarJam charges around 50 cents less with the same information provided.

- You can see examples of CarJam and PPSR reports for the same car search.

Dealing with Sellers - What You Need to Know and Do

To limit the risks, you must be assertive and cautious when buying a car with finance owed. Our suggested steps include:

- Ask the right questions: Inquire about the exact amount of finance owing, the lender involved, and the terms of the finance agreement. Ask for a settlement statement (this is an example of what one looks like) to verify the amount, and make sure you see the due date so there are no complications.

- Verify information: Don't just take the seller's word - you'll need to use the PPSR to check the car's financial status and contact the owner's lender to double-check the numbers.

- Discuss the payment process with the seller: You need to explain the process you'll follow. Most buyers transfer ownership simultaneously and pay the finance company and the seller directly. You need to agree on a process that protects your interests while remaining strong against any challenges from the seller.

- Check the legal ownership: Make sure the seller has the legal right to sell the car, especially in cases of joint ownership. You can do this instantly by checking the 'registered person' using NZTA's online service.

Buying a Car and Paying Off the Seller's Finance: Our Step-by-Step Guide to Protect Your Money

You need to proceed with caution, given the risks. Our step-by-step guide follows a proven path to protect your money and secure proper ownership:

1. Verify the Outstanding Finance:

- Before finalising any deal, use the PPSR to verify the lender(s) and then get permission from the seller to contact the lenders and confirm the exact amount of finance owed on the car.

- Why does this matter? Knowing the exact amount of debt (in dollars) upfront avoids surprises after you've committed to the purchase.

2. Negotiate the Sale Price and Deduct the Finance Owing:

- Agree on the sale price with the seller and then subtract the outstanding finance from it to determine what you'll pay the seller.

-

Why does this matter? This method ensures that the seller's equity in the car is separated from the outstanding debt and eliminates the risk of them taking your money meant for the finance company.

3. Draft a Formal Agreement:

- Prepare a written agreement (a popular template can be downloaded here) outlining the terms of the sale, including the payment split between the seller and the finance settlement.

- Why does this matter? A written contract provides legal proof of the agreed terms, protecting both parties.

4. Make Direct Payment to the Lender and Transfer Ownership Simultaneously

- Pay the finance owed directly to the finance company to clear the debt and simultaneously complete the ownership transfer process through NZTA.

- Why does this matter? This guarantees the loan is paid off, preventing the seller from misusing the funds. Transferring ownership at the same time as clearing the finance ensures the car is legally yours without any financial liabilities.

5. Verify Settlement and Clear Title:

- Confirm with the finance company that the debt is fully settled after payment. Check with the NZTA that you show as the owner and with the PPSR to ensure no finance is listed against the car.

- Why does this matter? This final step confirms removing any financial obligations and solidifies your legal ownership of the car.

Important: You must protect yourself at all times, legally and financially. We suggest the following:

- Get everything in writing: Draft a written agreement outlining all terms of the sale, including how and when the finance will be paid off.

- Use secure payment methods: Don't pay in physical cash; send the money to the seller via online banking. This gives you a record that can be invaluable in case of disputes.

Words of Warning from New Zealanders Who Have Bought Cars with Finance Owing

While it's not a dealbreaker to proceed with buying a car with finance owing, there are many risks and potential situations to be aware of, as these Car Loan Expert user stories outline:

1) The negative equity trap:

"A couple of years back, we were close to buying a car and decided to run a PPSR report on its registration. To our surprise, the report revealed an outstanding debt even though that wasn't mentioned. We asked the seller and were told it was $13,000, even though the car's sale price was around $10,000. This situation is known as negative equity.

The seller claimed he would use our payment, plus an additional $3,000 from his pocket, to clear the debt. This didn't make sense - why would someone pay more to settle a loan on a car they're selling? We realised he wouldn't pay anything, and we'd be legally responsible for the debt. Be very careful when dealing with anyone selling a car with money owing".

2) The 'forgotten' second loan:

"I bought a used car, aware of the small finance owing that the seller promised to clear with my payment. All seemed well, and I was driving around worry-free until a lender I'd never heard about phoned me about another (larger) loan still owing on the car. This was a detail the seller 'forgot' to mention, yet they gave this lender my number to 'work it out". This became an expensive mess - you must go deep into a car's financial history to avoid drama like this".

3) The lack of knowledge among buyers (as reported by a lender):

"Cars with finance often have security measures like immobilisers which the finance company can turn on at any time. Buyers need to talk to their seller's finance company before finalising any sale - it's scary how many buyers don't know this. It's an easy procedure - the buyer pays the lender to clear any outstanding loan, allowing the removal of security over the car. If you buy a car without contacting the finance company, you immediately risk the car being immobilised and repossessed".

4) The (often overlooked) joint ownership risk:

"I purchased a car with money owing, which the seller mentioned on the Trade Me listing. We agreed on a price, and I checked with the finance company about clearing the debt and made arrangements. However, I didn't realise the car was under joint ownership. After the sale, the co-owner, the (unsurprisingly in hindsight) seller's ex-partner, claimed they never agreed to the sale. This led to a legal dispute and a lot of hassle. My advice is simple - always verify the ownership status, especially in cases of joint ownership, to avoid legal problems".

5) The undisclosed mechanical faults issue:

"I focused so much on the finance aspect of buying my car (because I didn't want to get ripped off) that I neglected a thorough mechanical check. After buying the car, it wasn't long before the faults came up, and fixing them was expensive. I've learned the importance of not letting finance issues overshadow getting a full understanding of a car's overall condition".

However, it's not always bad news. In many instances, buying a car with finance owing is a smooth transaction, as this user experience outlines:

"Last week, I bought a car that had a finance owed. The seller was transparent about it. I contacted the finance company to verify the amount due and confirmed it was the only debt on the car. I then settled the difference between the sale price and debt (around $5,000) and paid off the finance company directly. Everything went smoothly".

Frequently Asked Questions

Can I buy a car with finance owing using my own car finance, and how does this process work?

Yes - you can use your car finance to buy a vehicle with existing finance owing. The general process is to get approved for car finance and then use the money to pay off the existing finance on the vehicle you're buying.

Your lender or broker will guide you through this process, ensuring all financial obligations are met before transferring ownership. This structured approach involves your lender settling the outstanding loan directly with the seller's finance company and paying the remaining balance to the seller.

What should I do if the seller is reluctant to provide a settlement statement from their lender?

If the seller hesitates to provide a settlement statement, it's a red flag. Insist on receiving this document, as it is essential to confirm the exact amount owed and ensure transparency. If the seller refuses, walking away from the deal is safer - don't be afraid to do this.

Is it safe to buy a car with finance owing from a private seller versus a dealer?

Buying from a dealer generally offers more security as dealerships are heavily regulated and ensure all finance is cleared before they sell a vehicle. The risk can be higher with private sellers, and it's the buyer's responsibility to do thorough checks. If you decide to buy from a private seller, we suggest rigorously following the steps outlined in our guide to protect yourself.

What legal recourse do I have if the seller doesn't clear the finance as promised after I've paid them?

If this happens, you'll need a lawyer, as it's a breach of contract law. To prevent this situation, always pay the finance owed directly to the lender rather than relying on the seller to do so.

How long does it typically take to transfer ownership of a car with finance owing once the loan is settled?

The time frame can vary, but typically, ownership can be transferred almost immediately once the loan is settled. Make sure to complete the transfer through NZTA once the finance company confirms that the debt has been cleared.

I've decided to avoid buying any car with finance owed. What are my options?

Choosing to avoid cars with outstanding finance is not uncommon, and your alternatives include:

- Buying from a dealer: Dealers typically handle all the paperwork and can guarantee that the cars they sell have no outstanding finance. Buying from a dealer can significantly reduce the risk of unresolved financial issues.

- Choosing a finance-free car: You can browse private sale listings and filter out vehicles with outstanding finance, or you can close the tab if your finance is owed.